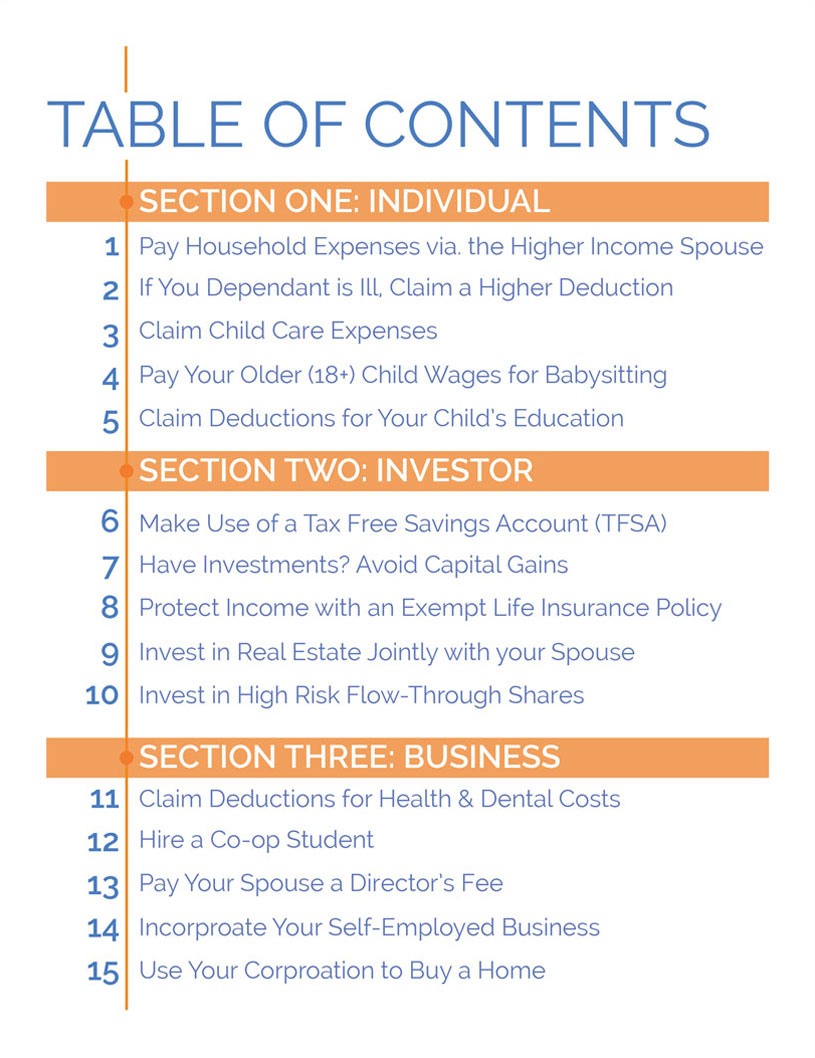

If there is a difference between you and your spouse’s income tax bracket, then this tax-saving strategy is ideal. This definitive and simple tactic calls for the higher income spouse to pay for the majority of the household expenses. This way, the lower-income spouse will be able to use his/her income for investment purposes.

Since the funds engaged in te investments belong to the lower-income spouse, the marginal tax rate applied to those investments will correspond to the lower income spouse. Hence, by using the lower-income spouse for investment purposes, you are saving tons of money that you would have originally be given to you in the form of taxes.

Under the Income Tax Act, those paying taxes have the right to claim a higher deduction if their dependent is unwell in a manner specified under the act. A specific set of symptoms and ailments, including neurological diseases, certain disorders, etc, give way for this higher deduction claim. This deduction claim raised further if the dependent suffering is a senior citizen.

Note, there are a few further conditions apply to this tip. The patient is not allowed to claim deduction on a separate basis and will not be reimbursed for his illness by an emloyer, third party, or an insurance company.

Furthermore, if the person paying the taxes has recieved only a certian amount as a compensation, the balance can still be claimed.

Did you know that the money you spend on your child’s child care can be reimbursed to a large extent? Childcare expenses are tax-deductible. However, the lower-income spouse is entitled to these claims only. Child care expenses include:

> Babysitting Fees

> PLASP Fees

> Daycare

> After-school programs

There is a cap on the total deductible amount that can be claimed. For children under the age of 7, you can claim up to $8,000 per child, per year. If your children are between the ages of 7 and 16, you can claim $5,000 per child, per year.

This tactic will allow you to claim a tax deduction for fees paid to your eldest child (18+) for babysitting your youngest child. As mentioned previously, childcare expenses - which include babysitting fees, are tax-deductible. Another advantage of this strategy is, ‘income splitting’.

The payments you are making to your older child will be included in his/her income for tax purposes. There is a high probability that the tax he/she would be paying on this income would be a negligible amount.

Another favorable aspect of this situation is that your child who is now earning income will be entitled to an RRSP contribution. Hence, this minor form of income splitting results in a beneficial situation for the whole family, in terms of beating the taxman.

The elimination of the federal education and textbook tax credit took has been effective as of Janurary 1, 2017. Don’t worry, the tution amount will provide you as well as your child a much-needed tax break. Wether your child is a full-time or part-time student, they can claim their tuition. If they do not have enough income, which is the case for many, no need to worry!

The unused tution can either be transferred or carried forward to the next year. Up to $5,000 of the tax credit can be transferred. This amount can be transferred to either the child’s parents, grandparents, spouse or common-law. This tip can not only help to reduce your child’s taxes, but also yours. Hence, being aware of claims that your family are entitled to can be surprisngly rewarding.

For the last several of years, Canadians were given the wonderful choice of opening a Tax Free Savings Account. To open a TFSA, you must be over 18 and have a valid SIN number. You should consider contributing to a TFSA because

> Income earned inside a TFSA is not taxable

> Withdrawls from a TFSA are not taxable

However, there is a limit on the amount you can deposit into a TFSA based on your “contribution room”. The CRA monitors the limits. Also, a TFSA can hold most investments such as mutual funds, bonds etc. It is recommended to use a TSFA to save for your child’s education.

Make investments in stocks, bonds or mutual funds that will appreciate in value - because you will save tax. The appreciation is only 1/2 taxable to you. For example, if you buy a stock for $10 per share and sell it for $18 per share, only 50% of the $8 gain will be included in your ncome. The other $4 (1/2) is tax-free!

Furthermore, if you own shares of a Canadian Controlled Private Corporation, you may be able to sell your shares and be exempt from capital gains on the first $850,000 of profit made on the sale. For example, Mr. Potato owns the shares of Potato Inc., a Canadian company. He sells his shares to Mrs. Tomato (unrelated) for $1,000,000. Mr. Potato will not have to include the first $850,000 of capital gains in his income, because of the lifetime capital gains exemption.

After deliberation with your financial advisor, consider using your life insurance policy as an investment strategy. Today, many life insurance policies follow an exemption rule. This means that an exempt policy allows a portion of the amount you pay as a premium to be deposited in a pool of investments free from tax.

This amount, along with the face value of the insurance policy can then be handed to your offspring or successor upon one’s death. However, in order to somehow be able to use this tax free pool of funds during your lifetime, you could potentilly use it as a collateal when borrowing funds.

Investing in real estate collectively with your spouse is a form of effective income splitting. Purchasing a house and then renting the property out will generate profits. By splitting that purchase with your spouse, it will result in a fifty/fifty split of the profits as well.

Hence the profits will not increase the amount of income earned for just one partner. It will be evenly distributed amongst both. Tax wise, it is smarter to split the amount as joint owners. This is because it will cut down the amount of tax your family has to pay.

Flow-through shares are designed to give investors a large amount of tax deductions, which are equal to, or almost as much as the original amount invested. The shares that you have invested in, allow tax deductions to be “flown” through the owner of the shares. The company issuing the flow through shares can renounce their expenses so that the owner can claim those expenses on his/her tax return.

The deductions that have been issued to the investor are not used in the same year. Flow-through shares can also be reduced by deductions the investor is able to claim.

In essence, by being able to deduct the full value of the initial investment (or close to it) on special kinds of shares, investors are able to earn back what they initially invested.

Your business can pay health and dental premiums to your insurance company, for you and your employees. If your business is your primary source of income and you are actively involved in its operation, then you are eligible to receive a deduction. A deduction is a claim that can be made to reduce your taxable income, it helps reduce your tax bill!

However, as the owner of the business, you must provide your employees the same health and dental benefits that you and your family receive. These benefits have to reasonable. In the case that you do not have any employees, you must make sure that the health and dental benefits are once again of a reasonable amount. It must be an amount similar to what you would receive if you were working for a third party.

If your business decides to hire a co-op student or an apprentice, you can claim a tax credit. A tax credit is different from a deduction. Receiving a tax credit will reduce your tax bill but not will it reduce your taxable income. It directly reduces your provincial and federal tax bill (dollar for dollar). As a business, you are entitled to receive a tax credit of up to 25% for corproations and 30% for small businessess. on salaries paid to co-op students.

There is a cap on the actual amount you can receive annually per co-op student. The maximum credit is $3,000 Canadian dollars per year. Through this tactic you can get reimbursed to a larger extent and benefit greatly as well from the skills of the apprentice or co-op student.

A director of a corporation helps oversee the management of your company. A director’s managerial activities include: attending director’s meeting, hiring officers for the company , approving & overseeing financial statemenets, declaing dividends, approving modifications to share capital of the corproation,

The performance of these services is called the ‘director’s fee’ and is paid directly to the director by the corporation. How is this relevant? You can appoint your spouse as the director and pay him/her to perform the relevant services for your corporation. If your spouse is in a lower income bracket, he/she will not be taxed heavily on the “fee” received from the corporation. In terms of saving taxes from the corporation’s side, the director’s fee is tax deductible, reducing the amount your company has to pay in tax.

If you are self employed and want to reduce your never-ending outflow of money in the form of taxes, consider incorporating. By legally incorporating your business, you are automatically reducing your soaring tax rate.

An incorporated business profits are only subjected to a tax rate of 11% (if Canadian controlled). Otherwise, the rate is 15%. , If you are a self-employed owner without an incorporated business, the profits of your business will be added to your personal income. This will increase your taxable income by a significant amount, potentially landing you in the highest income bracket.

This is one of the most effective tax strategies to cut down on the amount you pay as taxes. If you haven’t incorporated your business, it is best to speak to an experienced accountant immediately!

Instead of using your personal income to purchase a home, use your corporation to make the investment. How? Using an Employee Home Purchase Loan. As with any tax saving strategy, you should consult with your accountant before proceeding.

Step 1: Obtain a loan from your corporation on a tax free basis. Ensure that the mortgage is defined and that the home can legally be used as collateral.

Step 2:Pay a reasonable amount of interest, at least equal to the market rate of the interest.

Step 3:Ensure the term for repayment of the loan, is of a reasonable amount.

Step 4:Ensure you are an employee of your own corporation, receiving regular payroll and under a valid employment agreement.

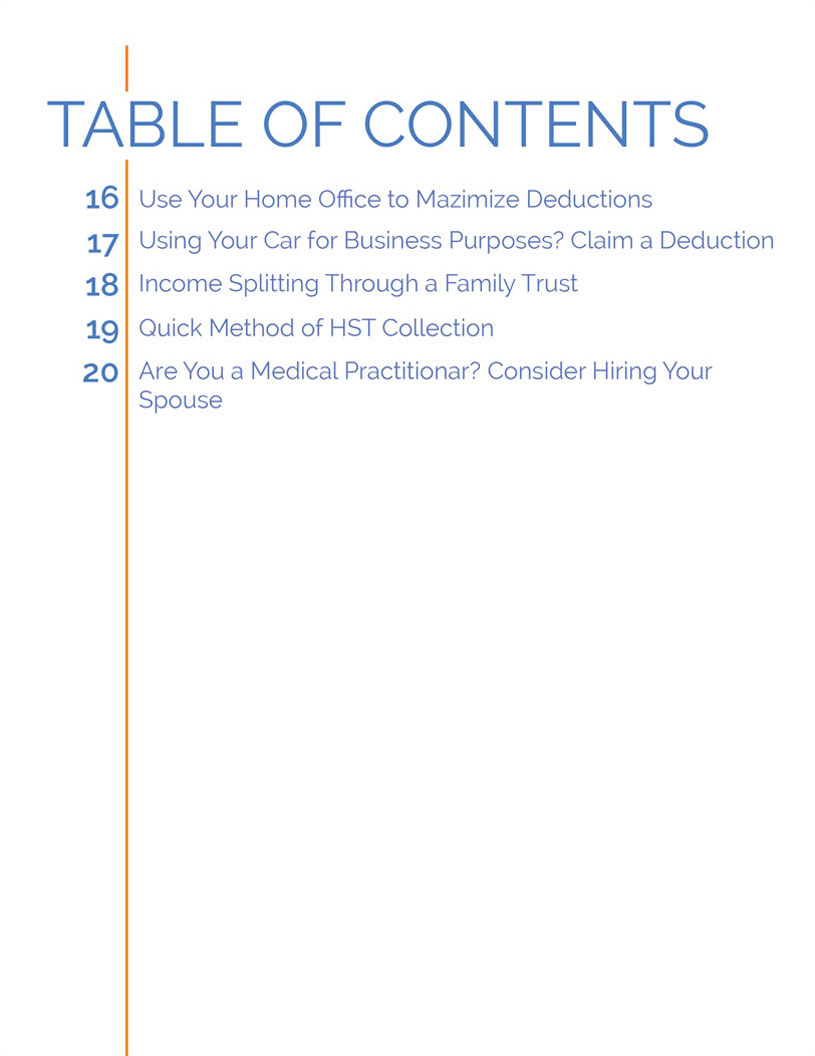

There are two taxable categories for home office: (1) your home is where you conduct the principal portion of your business (2) there is a specific location in your home (such as home office) that is exclusively used for your business. If your self-employment meets one of these criteria or both, you are allowed to start deducting your home expenses such as: interest on a mortgage loan, rent, utilities, repairs & maintenance.

Only a percentage of your home office can be claimed as a tax deduction. For example, if your home office makes up 20% of the square footage of your home, then only 20% of your house costs can be claimed. It is important to maximize your deductions as much as possible, so consider the following tip:

> Increase the amount of square footage your home office occupies

> Exclude square footage that is non-usable

Car expenses can be deducted to reduce your business income. Claimable automobile expenses include: lease costs (up to $800 per month), depreciatiion (calculated as 30% of the purchase price to a maximum of $30,000), parking fees and tolls your vehicle incurs, car washes, repairs, gas, insurance and auto loan interest.

You can only deduct the portion of your car expenses that relate to driving for business purposes. For example, if your business mileage is 80% of the total amount you drove your car then only 80% of your car expenses can be deducted. Note, keep a log book to track your business mileage!

Two things are certain in life, death, and taxes. When you pass away, your assets are deemed to be sold for tax purposes at their market value at that time. Any accrued gains become taxable to your estate. For example, if you bought a rental property for $100,000, and it increases in value to $1,000,000 upon your death, then your estate will have a capital gain of $900,000.

Half of this gain, $450,000, is taxable. Such a large tax bill can be a problem if your beneficiaries are unable to pay for it.

Forming a family trust to hold your assets will help you avoid taxes. However, assets placed in a family trust must be transferred to the beneficiaries of the trust within 21 years. This transfer occurs at the original purchase price of the asset and so a capital gain is not triggered. Capital gains tax will not be payable until your beneficiaries pass away or sell the assets.

The Quick Method is a simplified way of calculating net sales tax for HST purposes. The major advantage is that it results in reduced paperwork and easier calculations for small businessess. Note, this method is only available for a small business with annual revenue less than $400,000.

How this method works is you will charge your clients 13% HST on sales. If your business meets CRA requirement of less than $400,000 annual revenue you are only required to remit 8.8%.

CRA understands that it is important for small business owners to have capital reminaing. A major source of failures in new small businesses is they do not have enough cash available in the business. CRA is trying to help small business owners out by letting them keep a portion of tax collected.

The most common form of tax saving available to medical practitioner is through income splitting. Medical practitioners can hire their spouses and/or children and pay them a salary. This will allow some of the income earned in the business to be taxed at a lower marginal tax rate if your spouse or children have either no to very little income.

Important to note that the work must actually be performed and documentation must be kept. The pay should be an accurate representation of the work your spouse or child is performing.

Another form of Income splitting is making your spouse and/or children partial owners in your corporation. This allows you to transfer dividends to each member, elevating some of the tax burden.

About the Author

Allan Madan is a CPA, CA, and international tax expert. He is a graduate of the University of Waterloo where he earned a Masters Degree in accounting. He enjoys working with business owners, entrepreneurs and individuals. Allan has over 12 years of experience in public accounting. Prior to founding Madan Chartered Accountant in Mississauga, he worked for Deloitte, where he was an International Tax Manager. He has completed Parts 1 and 2 of the Canadian In Depth Tax Course, which is the most comprehensive tax training in Canada.

About the Company

![]()

At Madan Chartered Accountant, we know how important the experience is. We also know how critical it is to have someone in your corner that knows your unique situation. Your taxes are important to us, because they are important to you. Our knowledgeable and friendly staff will always take the time to go the extra mile. Among all the accounting firms in Mississauga, we’re special. Our unique size enables us to answer the most complex of problems, yet provide personal attention to all our clients.

Contact Us:

![]() 145 Traders Boulevard East, Unit 20 Mississauga, ON L4Z 3L3

145 Traders Boulevard East, Unit 20 Mississauga, ON L4Z 3L3

![]() amadan@madanca.com |

amadan@madanca.com |

![]() (905) 268-0150 |

(905) 268-0150 |

![]() (905) 507-9193

(905) 507-9193

© 2018 Madan Chartered Accountant Professional Corporation. All Rights Reserved.

SOCIAL CONNECT