U.S. sales tax: What Canadian businesses should know.

Allan Madan, CPA, CA

This webinar will provide you with an insight into the collection of sales tax and its potential implications.

The following subjects will be discussed:

- The Basics of U.S. Sales Tax

- Does Your Business Need to Collect U.S. Sales Tax?

- What States Do/Don’t Impose Sales Tax?

- When Do International Sellers Need to Collect U.S. Sales Tax?

- How to Get Sales Tax Compliant?

- Can I Avoid Penalties for Failure to Register & Collect Sales Tax Through a Voluntary Disclosure?

Introduction

We’ll start the webinar; first I’ll introduce myself. My name is Aborwanil Roy and I have been working with Madan Chartered Accountant for the last six months. Prior to that, I have worked with the big four for the last nine years. This is a great opportunity. Thank you for your time. Today, I will be presenting a webinar regarding U.S. Sales Tax. Sales tax has become a very big topic after the case between South Dakota v. Wayfair. Since then, our Canadian clients ask about U.S. Sales Tax – how to collect sales tax and what is sales tax. In this webinar I will explain to you what is U.S. Sales Tax, when do you need to collect U.S. sales tax and everything.

What is U.S. Sales Tax?

Sales taxes in the United States are taxes placed on the sale or lease of goods and services in the United States. It is governed at the state level and no national general sales tax exists. Forty-five states, the District of Columbia, the territories of Puerto Rico, and Guam impose general sales taxes that apply to the sale or lease of most goods and some services. These states also levy selective sales taxes on the sale or lease of particular goods or services.

Like Canadian provinces, each U.S. state can set its own sales tax rate. Unlike Canada, the U.S. has no national sales tax. Another difference: Within most states, there can be many different sales tax rates, as counties, cities, and other local taxing districts add their own sales taxes on top of the statewide tax rates. While most states allow additional local taxes, others don’t.

When a Canadian seller ships to a Canadian customer outside her home province, she adds the Canadian sales tax of the province to which she’s shipping. In the U.S., it’s not that simple. Some e-commerce orders are subject to sales tax and some are not. The difference has everything to with a little thing called nexus.

Most Common Question: “When do I need to start collecting sales tax?”

It is the merchant’s responsibility to collect online sales tax. Let’s discuss step-by-step at what merchants need to know to legally and efficiently collect and pay state sales tax on online transactions with their U.S. customers.

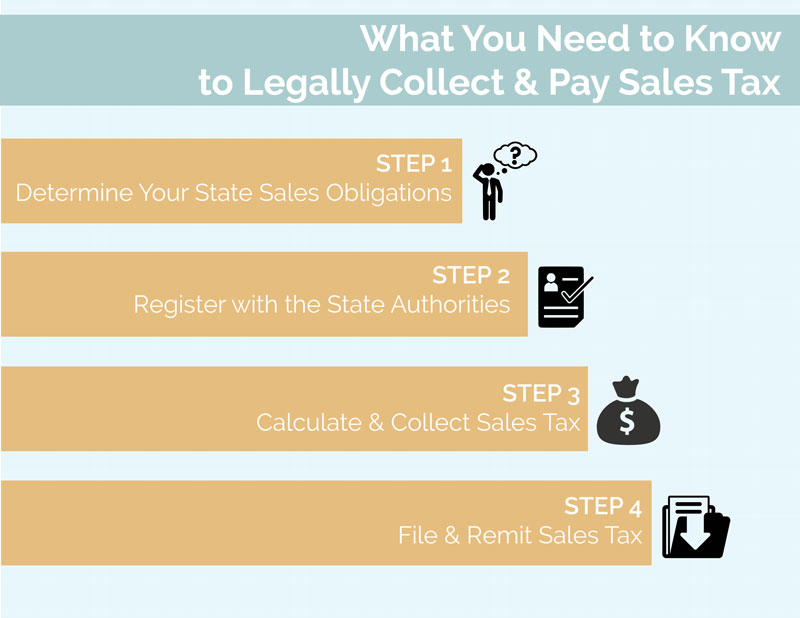

STEP 1: Determine Your State Sales Tax Obligations

JURISDICTION: First, figure out your sales tax obligations in the states where you do business. Currently, there are five states have no state sales taxes i.e Alaska, Delaware, Montana, New Hampshire & Oregon. In Alaska, local jurisdictions (cities and boroughs) are permitted to collect their own sales tax.

TAXABILITY: Not all products and services are taxable. As a general rule of thumb, tangible, non-essential goods are subject to sales tax. Products that are likely to be considered “essential” and thus not subjected to sales tax might include:

- Fresh and packaged food and ingredients (but not prepared food)

- Clothing (but not jewelry, bags, and other accessories)

- Prescription and over-the-counter medications

LEGAL COMPLIANCE: Online sellers can technically avoid collecting sales tax in states and localities that don’t explicitly mandate it. However, this is risky, as small merchants without dedicated compliance departments are unlikely to stay abreast of new state and local sales tax laws. The resources required to monitor the more than 10,000 U.S. sales tax jurisdictions are vast. For this reason, the best course of action for online retailers of any size is to assume they’re legally required to pay sales tax on transactions with buyers in all jurisdictions that levy sales tax.

STEP 2: Register With State Tax Authorities

Register with local revenue authorities wherever you plan to sell your product. In most states, the state department of revenue is responsible for collecting sales tax. State departments of revenue require certain information from businesses that wish to sell taxable products to residents, which include:

- Your Employer Identification Number (EIN), business tax ID, or both

- Your official business contact information, including the registered agent’s mailing address

- Your NAICS code

There are various ways to register. You can visit your state online registration and follow the procedure or you can register by email.

Once you have your state sales tax permit, you can legally sell and collect sales tax in that jurisdiction. Moving forward, you’ll need to mind any ongoing compliance requirements, such as reporting and filing state sales taxes by the applicable deadlines.

STEP 3: Calculate & Collect Sales Taxes

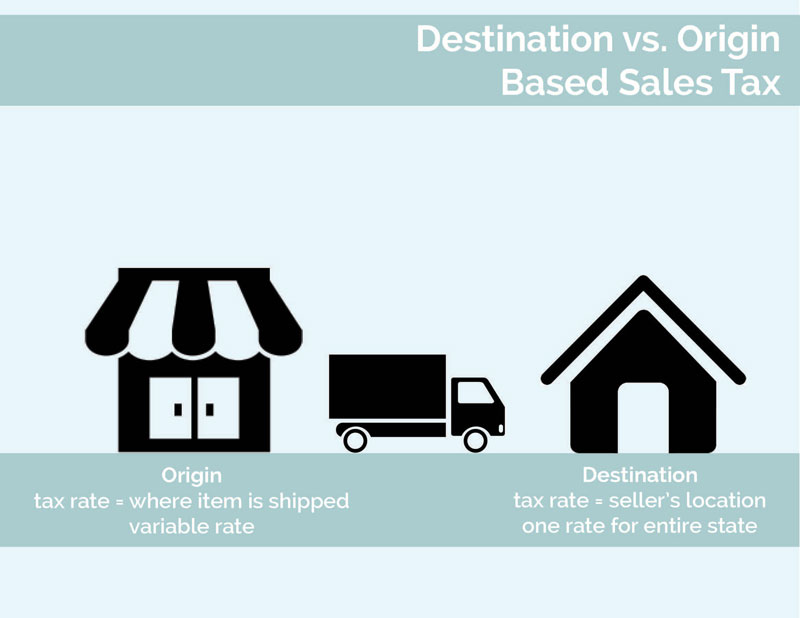

The United States is a mixture of thousands of state, local, and special tax districts. Fortunately, you have no personal obligation to keep track of the various tax rates charged in all the jurisdictions in which you sell. Virtually, every e-commerce suite is equipped to do this on your behalf. Even if they don’t need to calculate local tax rates manually, online sellers can benefit from understanding the distinction between origin- and destination-based taxation.

About a dozen states, including Texas and Illinois, impose origin-based taxation, which is the simpler of the two options for sellers. Under origin-based regimes, buyers always pay sales tax at the rate charged at the origin point.

Most states impose destination-based regimes. Destination-based taxation is more predictable for buyers since it means they always pay the same sales tax rate. For sellers, however, destination-based regimes necessitate more compliance and auditing. Even if your e-commerce suite automatically collects sales taxes at destination rates, you’ll want to spot-check actual collections against the rates published by state revenue authorities to confirm accuracy.

STEP 4: File & Remit Sales Taxes

Assuming you’re using an e-commerce or accounting suite that automatically tracks sales tax collection, you should have an accurate running total of your sales tax receipts at any given point in time.

Filing State Sales Taxes?

Business sales tax filings help state and local revenue departments keep tabs on merchants selling taxable goods and services within their jurisdictions. This is essential for budgeting and tax enforcement. Newer merchants familiar only with the personal tax filing process might be surprised to learn that businesses are not always required to remit funds with sales tax filings.

A sales tax return without an accompanying remittance is known as a “zero return.” Pay special attention to zero-return requirements! Not all jurisdictions require zero returns, but those that do are serious about collecting late fees and penalties from businesses that fail to abide.

What States Do/Do Not Impose Sales Tax?

There are five states that don’t have a sales tax, which are:

- Alaska

- Delaware

- Montana

- New Hampshire

- Oregon

Currently, 45 states plus the District of Columbia impose a general sales tax.

State & Local Sales Tax Rates

There are forty-five states and the District of Columbia collect statewide sales taxes. Local sales taxes are collected in 38 states. In some cases, they can rival or even exceed state rates. The five states with the highest average combined state and local sales tax rates are Tennessee (9.47%), Louisiana (9.45 %), Arkansas (9.43%), Washington (9.17%), and Alabama (9.14%).

When Do Canadian Businesses Need to Collect U.S. Sales Tax?

Just because you are manufacturing in Manitoba or crafting in Saskatchewan doesn’t mean you don’t need to collect and remit sales taxes on the orders you ship to customers in the United States. If you have sales tax nexus in the state where your customer is located, you must collect and remit sales tax on that order.

Sales tax nexus at its most basic is a physical presence in a state, such as a business location. In the era of online shopping, the definition of nexus has become more nuanced. You have US sales tax nexus, even if you are based in Canada if you have a physical location in the U.S. such as an office, a store, or a warehouse. Remote employees create nexus in the U.S. state where they live. If you have an employee, such as a sales rep, who travels in the US, the time your employee spends in a particular state can create nexus, even if it’s just a few days a year. If you sell through Amazon FBA, your merchandise stored in an Amazon fulfillment center could also create nexus. Track where your FBA inventory has created U.S. sales tax nexus through Amazon inventory reports.

Nexus doesn’t stop at physical locations and employees. Affiliate marketing nexus, also known as click-through nexus or Amazon laws, is a concept that has been adopted by a number of states, starting with New York. Aimed at getting Amazon to pay state sales taxes, these laws create nexus when an affiliated website generates a certain amount of sales for your business.

For instance, you sell cowboy hats out of Winnipeg and you enter an agreement with the Cowpoke Journal to promote your goods and send customers to your site. You give the Cowpoke Journal a commission for every referral that turns into a sale. The person who runs the site is based in Arkansas, which has a click-through nexus law. If your affiliate relationship generates at least $100,00o in sales during a 12-month period, you’ve got U.S. sales tax nexus in Arkansas. Like most other US sales tax rules, the regulations governing click-through nexus vary from state to state.

Exemptions from US Sales Tax?

There are many transactions between Canadian sellers and U.S. customers where there’s no need to collect and remit U.S. sales tax. If you don’t have nexus in the customer’s state, you don’t need to add US sales tax to the order. Likewise, if your sale is tax-exempt (a wholesale order or a sale to a non-profit- if it’s in a state where non-profits are exempt from sales tax), there’s no need to collect U.S. sales tax.

How to get Sales Tax Compliant?

We have already mentioned in previous slides that before you can start collecting U.S. sales tax, you need to register with each state where you have nexus. Some states make it easy by allowing you to do this through an online form. Once you have registered, you will be required to fill out regular sales tax returns. There are some software’s which can help you file your sales tax return and be compliant.

Can I Avoid Penalties for Failure to Register & Collect Sales Tax Through a Voluntary Disclosure Agreement (VDA)?

After nexus determination, state registrations are needed to formally collect and remit sales and use tax, but one question may lead to handling registration in a different manner. Registration forms require a company to disclose when it began “doing business” in the particular state(s), and if the company has been operating in that state for a long time period, a Sales Tax Voluntary Disclosure Agreement (VDA) may be a better option.

A VDA is a way for companies to avoid fees and criminal charges for unreported taxable income. Companies may innocently overlook income they should have filed, but without the help of a Sales Tax Voluntary Disclosure provider, they can incur serious penalties should the failure to report be discovered.

Specific rules vary from state to state, but sales tax voluntary disclosure through a VDA is generally a great way to ensure your company is compliant with the State Department. If you have resisted the sales tax voluntary disclosure program for fear your failure to report may be viewed as criminal, you should be aware that by law, the information you provide as part of a VDA program cannot be used against you — unless you violate the VDA terms.

A VDA is only for taxes owed but not previously reported. If you already filed a return but simply have not paid some or all of the taxes you owe as per that return, you are still responsible for any late fees or penalties on those taxes.

Disclaimer

The information provided on this page is intended to provide general information. The information does not take into account your personal situation and is not intended to be used without consultation from accounting and financial professionals. Allan Madan and Madan Chartered Accountant will not be held liable for any problems that arise from the usage of the information provided on this page.

ABOUT THE AUTHOR

ALLAN MADAN

CPA, CA

Allan Madan is a CPA, CA and the founder of Madan Chartered Accountant Professional Corporation. Allan provides valuable tax planning, accounting and income tax preparation services in the Greater Toronto Area.